Expanding access to alternative investments in 401(k)s

Policymakers are examining ways to give 401(k)s and other defined contribution retirement plans more access to alternative assets, which include investments in private credit, hedge funds, private equity, and real estate.

These assets can strengthen returns for retirement portfolios over time by improving diversification and reducing volatility. Pension plans, another common retirement option, have long used alternative investments alongside stocks and bonds to deliver secure retirements for millions of essential workers, including teachers, firefighters, and nurses.

Key resources

Why are 401(k) plans interested in adding alternative investments?

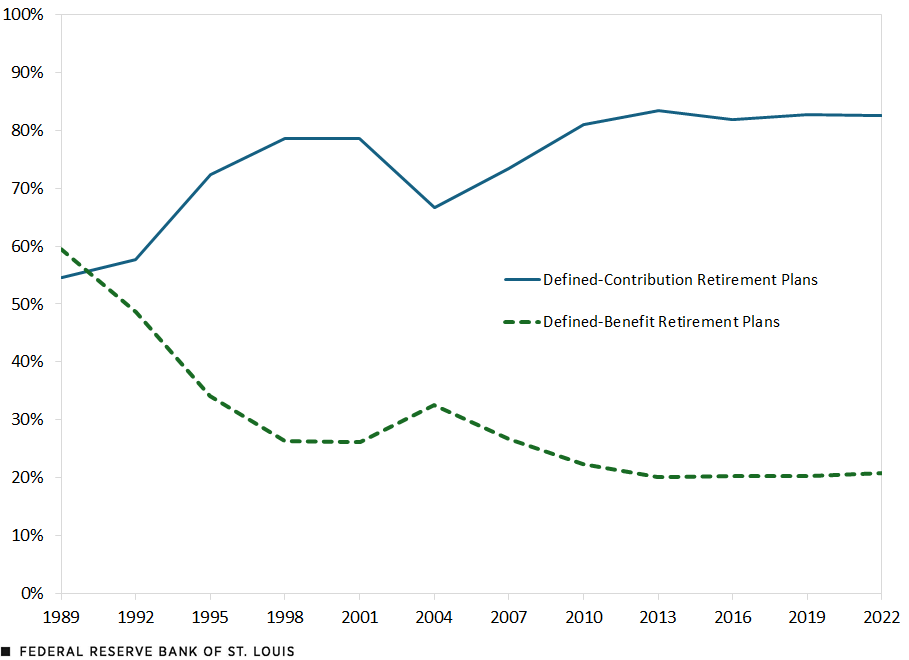

More Americans now save for retirement through defined contribution plans, such as 401(k)s, while traditional pensions cover a shrinking share of the workforce.

At the same time, private markets have grown significantly over the past several decades, with companies staying private longer and an increasing share of economic activity now occurring outside public markets.

Most 401(k) plans have been largely limited to publicly traded stocks and bonds, while pension plans have incorporated alternative investments to benefit from the growth of private markets. This difference has created an access gap between investors with pensions and individual retirement savers.

Policymakers are working to modernize the rules so 401(k) participants can benefit from the same diversified investment tools that pensions have used for years, with appropriate safeguards and fiduciary oversight.

How do alternative investments improve retirement portfolios?

Long-term retirement saving depends on diversification. A mix of different types of investments helps smooth returns over time and reduces the impact of market downturns.

For decades, many retirement portfolios have followed a “60/40” model — roughly 60% in stocks for growth and 40% in bonds for income and stability.

Recent periods of market stress have shown that stocks and bonds can decline at the same time, underscoring the importance of broader diversification.

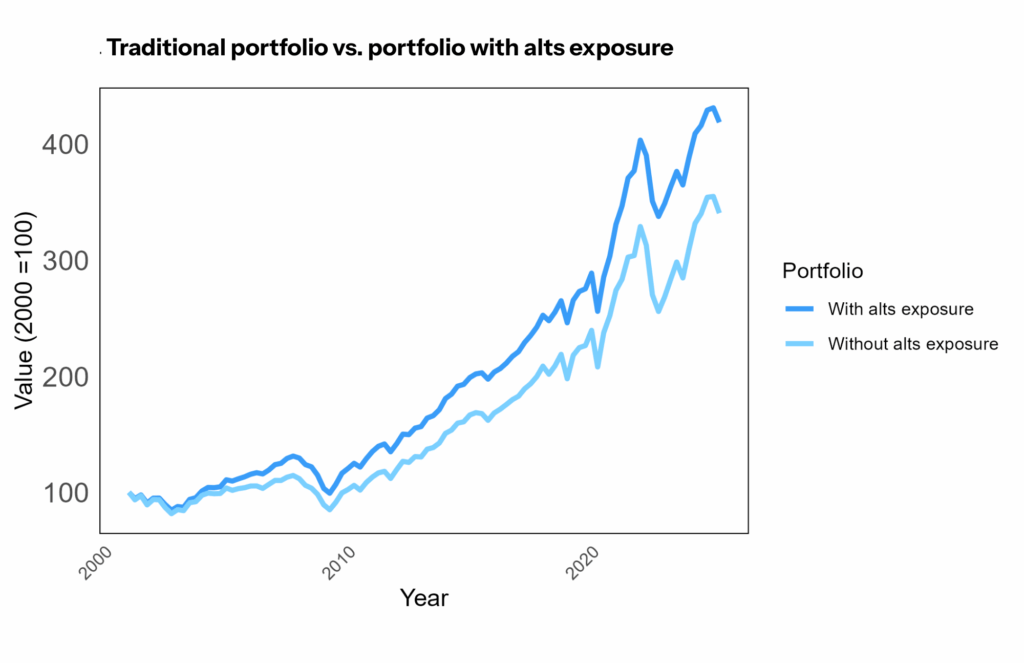

Alternative investments can provide an additional source of diversification. They allow portfolios to include assets beyond traditional public stocks and bonds, which can help reduce volatility and improve long-term risk-adjusted returns.

Research shows portfolios that include alternative assets have delivered stronger long-term performance than portfolios limited to stocks and bonds alone.

Adding alts to your 401(k) mitigates risk, reduces volatility, and makes it more resilient – Analysis showing how alternatives improve portfolio resilience across market cycles.

Adding alternative assets materially improves portfolio performance in a 25-year back-test – A long-term back-test demonstrating improved performance and risk-adjusted returns when alternatives are included.

MFA principles for alternatives in 401(k)s

Expanding access to alternative investments in 401(k) plans should follow a clear, principles-based framework that prioritizes savers and fiduciaries. Any expansion of access should meet the following standards:

- Retirement savers benefit from more choice. A wider range of investment options, including alternatives, can help 401(k) participants meet long-term savings goals when offered through diversified funds.

-

Rules should be flexible and strategy-neutral. Regulators should set clear guidelines without favoring or discouraging specific investment strategies.

- Strong fiduciary oversight matters. Professional investment managers play a critical role in managing risk and acting in the best interests of plan participants.

- Fees should be judged in context. Costs should reflect the services provided, the complexity of the investments, and the needs of each plan and its participants.

- The legal environment should support good-faith decisions. Excessive litigation can discourage plan sponsors from offering well-designed investment options that benefit savers.

FAQs

What's the difference between a 401(k) and pension

A 401(k) is a defined contribution account where workers contribute part of their paychecks, often with an employer match, to a tax advantaged investment account. The money is invested, with long-term returns determining the account holder’s retirement income. About 70 million Americans have a 401(k), making it one of the most common ways that workers save for retirement.

A pension, often called a defined benefit plan, promises a guaranteed monthly payment in retirement, usually based on salary and years of service. The employer funds and manages the plan. Roughly 19% of U.S. workers are estimated to participate in a pension plan, making them far less common than 401(k)s.

Why don’t 401(k) plans currently offer alternative investments?

Most 401(k) plans have traditionally focused on publicly traded stocks and bonds, which were the primary investment options when the modern 401(k) system developed in the 1980s. Regulatory uncertainty has limited broader adoption of alternative investments, even as pensions have incorporated them for decades.

How would alternatives be offered in a 401(k) plan?

Alternatives would typically be included within diversified, professionally managed funds — such as target date or asset allocation funds — rather than as standalone investment options. Plan fiduciaries would determine appropriate allocations.

Will alternatives in my 401(k) have fiduciary oversight?

Yes. Plan sponsors and investment managers must act in the best interests of participants and follow established fiduciary standards when selecting and monitoring investments.

Would alternative investments replace stocks and bonds?

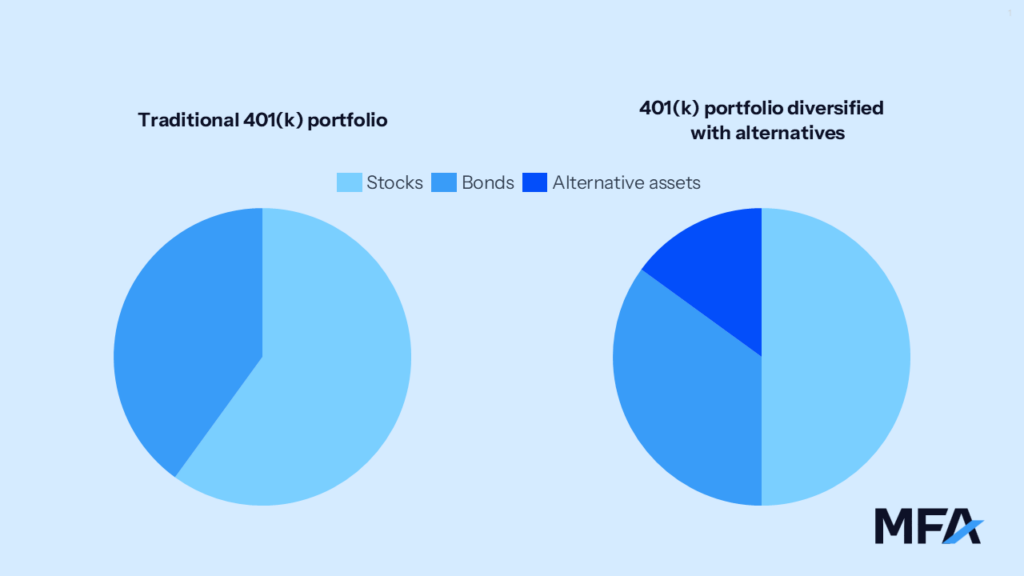

No. Alternatives are designed to complement traditional stocks and bonds by broadening diversification within a retirement portfolio. Alternatives made up 15% of the example portfolio used in MFA’s research, alongside 50% stocks and 35% bonds.

If my 401(k) plan sponsor decides to add alternative assets, will I have to invest in them?

No. Plan sponsors typically offer a range of options, many of which will likely not include alternative investments. Participants retain control over their investment choices and can select the options that best align with their retirement goals and risk preferences.

If my 401(k) invests in alternative assets, will I be able to get my money back when I want it?

Yes. 401(k) plans are structured to provide participant liquidity under standard plan rules. Alternatives included within diversified funds would be designed to operate within those same liquidity frameworks.