Published

April 8, 2026

Topic

Fueling Small and Midsize Business Growth, Private Credit

Type

MFA Report

Share

Why is valuation important?

Valuation is the process through which private fund managers determine the worth of the investments in their portfolios, making it fundamental for both fund investors and the asset-management business. Some assets such as stocks, bonds, and exchange-traded funds (ETFs) trade frequently and therefore have observable shifts in market prices each day. Others that trade infrequently, or not at all, require well-established valuation frameworks to determine their value when needed.

Valuations are used to assess fund performance and to help investment advisers monitor and manage portfolio positions. Managers apply disciplined methodologies designed to reflect fair value. They also rely on formal valuation policies and procedures, internal controls, independent third‑party pricing services where appropriate, transparent disclosure of valuation practices, and strong corporate governance oversight to promote consistency and reliability.

Unlike mutual funds, private funds do not offer daily liquidity. Many private funds hold illiquid investments and may not provide liquidity to investors for several years, eliminating the needs for daily pricing that exists for mutual funds. Valuation remains critical, however, to ensure investors receive accurate payouts upon redemption or at a fund’s closing. Robust practices are therefore essential to best determine fair value.

Best practices that support accurate and objective valuations include:

-

Managers adhere to robust valuation procedures, implement strict internal controls, and often rely on independent consultants for objective price estimates.

-

Managers provide investors with comprehensive disclosures of their valuation and governance practices.

-

Managers are accountable to the U.S. Securities and Exchange Commission (SEC) and state securities authorities.

How is valuation used to determine fund performance?

Fund performance is measured by looking at the total value of a portfolio of investments over time. For private funds, this includes both the cash that has already been returned to investors and the estimated value of the private investments that remain in the portfolio.

Because many private investment funds last several years, performance cannot be judged solely by early cash outcomes. Valuations help show how a private fund’s portfolio holdings mature at different points in the fund’s life by providing a snapshot of the remaining investments’ value at that time.

By reviewing valuations over time, investors and advisers can better understand how the value of a portfolio comprised of private loans or other assets changes as investments mature, perform, or are repaid.

How does valuation work?

Valuing publicly traded securities like stocks and bonds is straightforward, as fund managers rely on each day’s closing market prices. Valuing less liquid assets such as real estate, private credit loans, or stakes in private companies is harder because they do not trade on public exchanges. In some cases, managers reference recent transactions from comparable investments. When reliable market data is unavailable, they estimate the asset’s fair value using rigorous accounting standards and established valuation methodologies, often with input from independent experts.

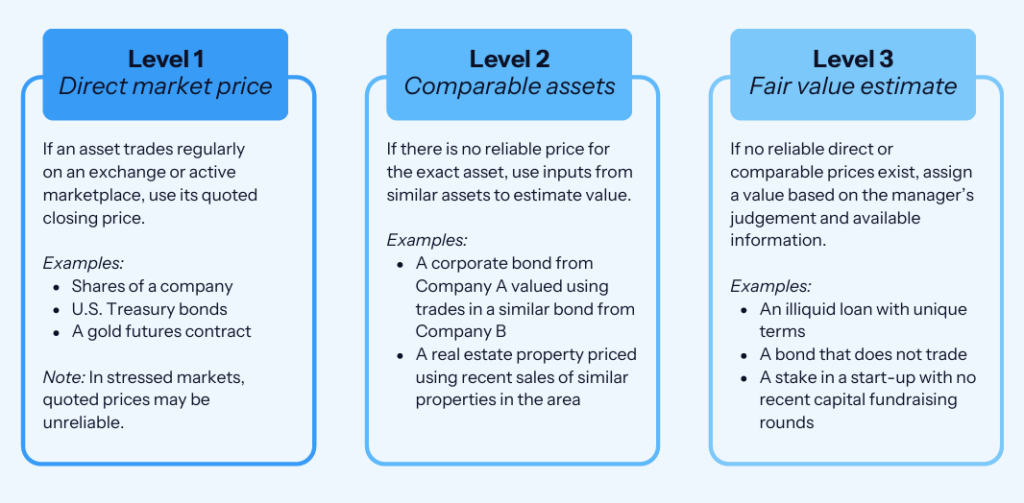

Accounting authorities use three distinct valuation levels based on the availability of market prices or other “inputs,” which guide how illiquid assets are valued.

Valuing Level 3 assets

Robust valuation procedures

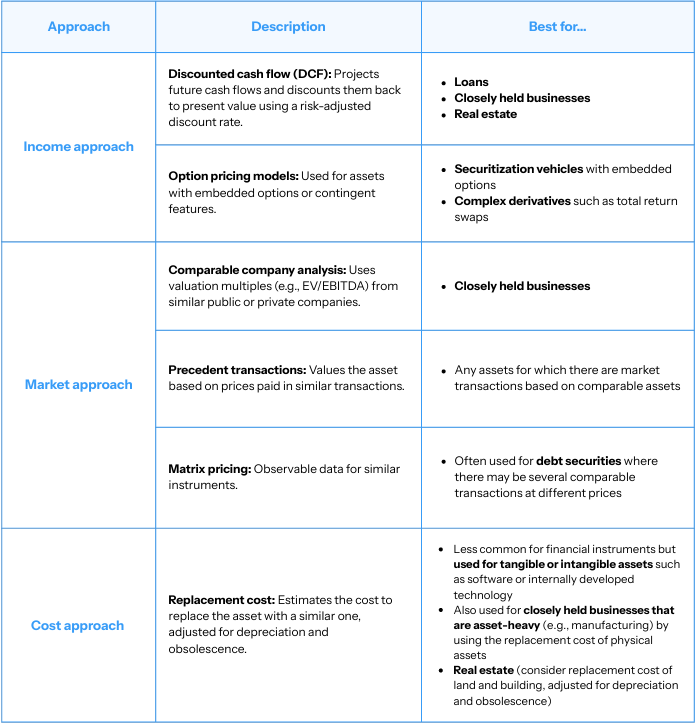

Given that Level 3 assets lack observable market prices, their valuation relies on professional judgment and carefully applied analytical methods. Three primary approaches—the income, market, and cost approaches—are applied depending on asset type and available data. The table below summarizes these approaches and their typical applications.

Valuation differences across similar loans

-

Different methods: The existence of multiple accepted methodologies helps explain why two distinct private fund managers might assign different values to the exact same asset. This variability does not necessarily indicate inaccuracy or bias. It may simply reflect differences in approach—such as one manager applying a discounted cash flow analysis while another references comparable private company valuations.

-

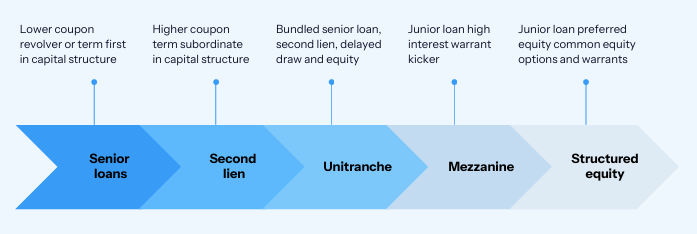

Similar-looking loans can be quite different: With Level 3 assets, it is important to recognize that comparisons are often not “apples-to-apples.” Each specific loan may have varying underlying factors. It is possible that multiple loans made to the same borrower have different valuations even though the loans appear to be the same. That’s because characteristics can vary considerably. Rights, terms, and structural features often vary, such as rates, priorities in bankruptcy/ insolvency, collateral, and added incentives (e.g., equity stakes):

Such variables can result in a different valuation for the different loans, even though the loans may look similar. When comparing valuations for the same borrower, it is critical to analyze the specific rights, terms, and structural features of each loan to ensure an “apples-to-apples” comparison, recognizing that differing methodologies may also contribute to valuation differences.

Safeguards to ensure consistent, reliable valuations

Strict internal controls

Valuation committees, formally approved and reviewed annually by the manager’s – or the fund’s – board or leadership, provide independent oversight of the valuation process.

Portfolio management, trading teams, and legal and compliance departments work together to support, monitor, and verify procedures, ensuring consistency, objectivity, and accountability throughout.

Use of third-party valuation agents (a.k.a. pricing services)

To ensure accuracy, managers frequently rely on one or more independent, third-party valuation agents or pricing services. For instance, to help value private credit loans, valuation agents maintain historical loan databases and have developed sophisticated pricing models based on loan data and other inputs specific to the borrower and the underlying collateral.

Managers will carefully compare these third-party valuations against internal models and other sources. If the fund manager overrides the valuation agent’s pricing, the manager bears the burden of demonstrating that their valuation is more accurate under the circumstances. Significant divergences from third-party valuations or repeated overrides can raise concerns among investors and create potential litigation or regulatory risk.

Disclosures of valuation procedures

Fund managers disclose their valuation procedures to regulators and the public through Form ADV, which must be filed when firms register with the SEC.

Investors also receive detailed information about the valuation process through the fund’s offering and subscription documents. Moreover, investors assess valuation practices through due diligence, asking detailed questions about a fund manager’s valuation process during manager selection.

Legal and regulatory safeguards for valuation integrity

Investment managers are fiduciaries to the funds they manage and are subject to private litigation and enforcement actions by the SEC and state securities authorities if their valuation practices are inconsistent with those disclosed to investors.

Conclusion

Valuation plays a key role in how private funds assess performance, manage risk, and maintain investor confidence. The process of valuing illiquid assets involves professional judgement and carefully considered, rigorous processes. Fund managers typically follow established procedures, consult independent experts, and disclose their valuation practices to support transparency and consistency of pricing.

Related Research

July 13, 2026BlogExternal Research

Private Credit Strengthens Financial Stability, New Research Shows

June 25, 2026BlogCommissioned Report

Leverage drives the economy. It’s time we understand it better.